Congratulations to Mike & Torrey.

They bought a beautifully remodeled home in the Cole/RINO neighborhood this summer.

Denver Residential Real Estate

Congratulations to Mike & Torrey.

They bought a beautifully remodeled home in the Cole/RINO neighborhood this summer.

Disclaimer: We are not lenders, we are not financial advisors, we are not accountants, we are not attorneys.

Do you have home equity? Wondering how you can use it to your advantage?

So you bought a home a few years ago and have EQUITY! The value has gone up, but how can you use the gain in value to your advantage? Home value is not a liquid asset, but with a tool called a Home Equity Line of Credit (HELOC) you can utilize your equity on your primary residence without selling your home. There are several institutions that offer this type of credit and we’ve done some shopping around for you to help you pick the best program.

We called the top five banks that were recommended for their HELOC programs. We gave all of them the same scenario. The given scenario was: The homeowner’s agent said their house is worth $500K. The owner purchased the home for $400K two years ago and currently has a loan on the property for $380K. Their credit score is 750, income is $60K, debt = $2000/m for mortgage, $250/m car payment, $3000 in credit card debt.

Disclaimer: Rate fluctuate everyday and are based on your personal scenario, the rates below are just estimate for demonstration. Rates were as of July 2019.

The amount of money you can borrow for a HELOC will be calculated by multiplying the current home value by the percentage (typically 80-90%) and subtracting the current loan on the property. EX: $500K (current home value) x .89 (loan to value) = $445K – $380K (loan on home) = $65,000

Here is how we would rank the HELOC programs that we researched.

1. Bellco – 80% at a fixed 3.99%, 80-90% at a fixed 4.49%

2. Red Rocks – 89% at a 5.5% adjustable rate

3. Vectra – 85% at 5.35% to 5% adjustable

4. US Bank – 85% at 6.3%

5. Chase – 80% at 9.38%

Here are some assumptions you can make about most HELOCs…

1. Will have an adjustable rate and will fluctuate with the market rate during the term of the loan. BELLCO is running a special right now on a FIXED RATE HELOC

2. Can only be taken out a your primary residence

3. Payments are typically interest only

4. You will have to pay for an appraisal, closing cost, and it will usually benefit you to open an account at the institution

5. Unlike a second mortgage, a HELOC gives you access the the equity but you don’t have to pull out a lump sum

So now that you know what some local banks are offering, let’s think through a few scenarios on how you could utilize a HELOC. We must mention, HELOCs are NOT bottomless piggy banks to fund affluent lifestyles that you really can’t afford. The frivolous use of HELOCs in part lead to the Great Recession in 2008.

1. Moving Up – Many homeowners utilize the equity they have in their first home to purchase a second home. In Denver’s competitive housing market it can be extremely difficult to purchase a new home with a contingency to sell your current home. Also, many families don’t want to sell their current home without having a replacement home under contract. HELOCs are a solution many buyers are utilizing to avoid this dilemma. You can make an non-contingent offer, use funds from a HELOC as the down payment on your replacement property, and close on your new home THEN list your first home. With the proceeds from the closing of your first home you will have to pay off the first mortgage and HELOC in full. All the banks we spoke with confirmed that a HELOC can be used for anything… including the purchase of another home, but MAKE SURE TO CHECK WITH YOUR LENDER!

2. Home Improvement – Are there aspects of your home that you would like to improve? If so, a HELOC might be a great option for you. A HELOC allows you to borrow against the equity you already have in your home. Allowing you to finance these larger purchases over time instead of in one lump sum. Keep in mind that many of these rates are typically not fixed and payment are interest only, so having an established payment plan that includes a strategy to pay down the principle will be in your best interest. When considering home improvements, be sure to be mindful and discuss your improvement plans with your trusted real estate agent. Your agent can help you navigate what improvements are going to bring the most value back into the home when you sell. Take it from us, there is nothing more discouraging than putting a lot of money into a home that does not increase the value.

3. Consolidating other higher interest loans – Have you evaluated the interest rate on your student loan and credit cards? It can be extremely difficult to pay off high interest loan debt if you interest rate is 19.24% (average credit card interest rate). It might benefit you to use a HELOC to pay off debt with a higher interest rate.

We can help you with any real estate questions including: How much is my house worth? What is the best strategy to buy a second home? What renovation projects give the best return on investment. Call us: 303-720-8491

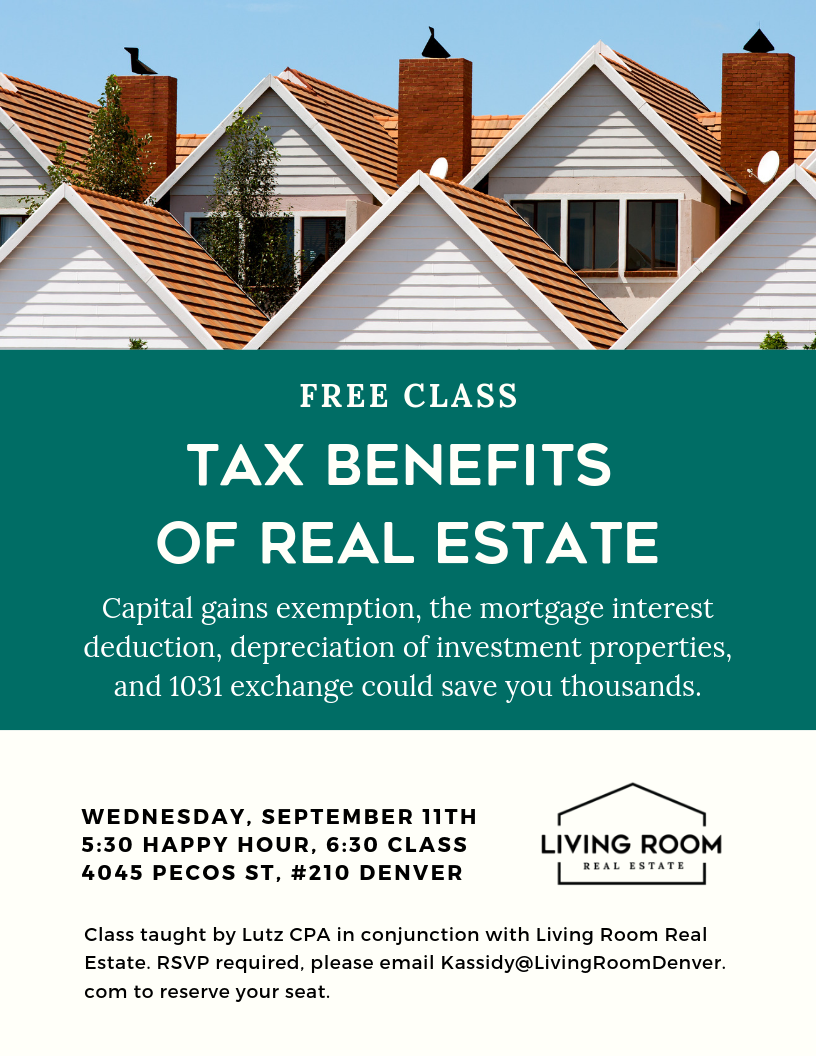

Capital gains exemption, the mortgage interest deduction, depreciation of investment properties, and 1031 exchange could save you thousands. Class taught by Lutz CPA in conjunction with Living Room Real Estate. RSVP required, please reserve your seat on EventBrite.com.

5:30 pm – Networking, Happy Hour and light food served

6:30 pm – Class, followed by Q & A

We would love to have you join us tonight at the Irish Rover

54 S Broadway, DENVER 80209

RSVP to Taylor@LivingRoomDenver.com

July Market Report was posted. Looking good Denver.

Hannah & Brandon, Edgewater

Kassidy Benson, Buyer Representative

Read their client testimonial here

Lauren & Forrest, Athmar Park

Kassidy Benson, Buyer Representative

https://www.zillow.com/homes/579-S-Quivas-Street,-Denver-CO-80223_rb/13357205_zpid/

Mark your calendar. I hope you can make it!

Meet at the local watering hole and learn the neighborhood characteristics, market stats and amenities.

After a drink, we will look at one or two houses for sale in the neighborhood.

HAPPY HOUR!

Thursday, JUNE 14th at 6PM

Plimoth, 2335 E 28th Ave, Denver, CO 80205

in Denver’s Skyland neighborhood.

A great way to get out and get a feel for the different neighborhoods is to check out the local neighborhood Farmer’s Markets. These are my favorite farmer’s markets around Denver.

Cherry Creek Fresh Market

Saturdays, May 4th – Oct 26th 8AM- 1PM

Wednesdays, June – Sept 25th 9AM 1PM

Union Station Market

Saturdays, May 11th – Oct 26th 9AM- 1PM

South Pearl Street Farmers Market

Saturdays, May 19th – Nov 17th 9AM- 1PM

RiNo Fresh Market

Saturdays, June 15–Oct. 12, 2019 9AM–1 PM

Highlands Square Farmers Market

Sundays, June 2–Sept. 29, 2019, 9AM– 1PM

City Park Fresh Market

Sundays, June 2–Oct. 27, 2019, 9AM –1PM

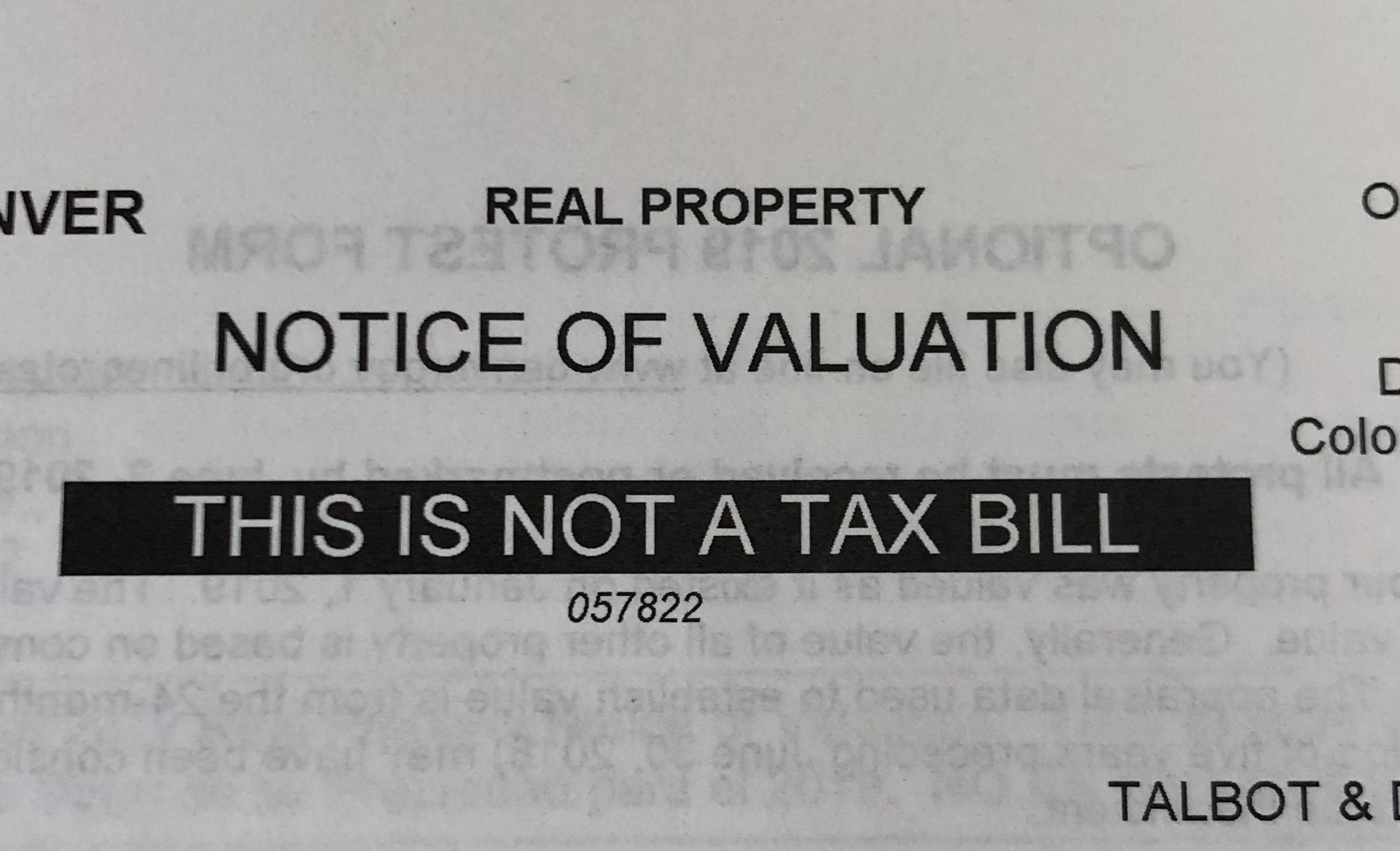

Did you get your “notice of valuation” from the city of Denver? The city is working hard to accurately value your property so they can fairly tax households throughout the county and raise money for public services and projects. Denver recently launched a program called the Denver Tax Receipt where you can actually see exactly where your tax dollars go, I highly recommend checking it out!

Your valuation should be close to you Zestimate or actual market value of your property. If you are the worst house on the block, your property value probably came in higher than the actual market value. If the valuation is not accurate, you have the ability to protest it with the city by June 3rd. Please email me if you need help protesting this value (kassidy@LivingRoomDenver.com).

Did you know Colorado is ranked 5th nationally for most affordable property tax valuations? Our taxes here are actually very low. The median household in Colorado is paying about $1500 in taxes per year in property taxes. The highest state property taxes are in New Jersey where residents pay $7840/year. California has a bad reputation for high taxes, but residents are paying about $3414/year. The red state of Texas actually has very high property taxes, ranked 45 of 50 making it one of the most expensive state property taxes. We looked at tax rates at a state level, but remember that your actual taxes will be determined by the combination of state, county, and city taxes.

Once I understood where your taxes go by using the Denver Tax Receipt, I felt very proud to be contributing to fund the important services that make our great city run. I’m also grateful to live in a state that has affordable taxes when compared to other places. It’s a whole new perceptive once you start looking at the big picture!